ARCHITECTURE, ENGINEERING, CONSTRUCTION RESEARCH & DEVELOPMENT TAX CREDIT

- Architecture

- Civil Engineering

- Electrical Engineering

- Environmental Engineering

- Mechanical Engineering

- Product Engineering

- Structural Engineering

- General Contracting

- Electrical Contracting

- Mechanical Contracting

- And More

Maximizing your opportunity for success

Although architecture, engineering and construction firms were previously excluded from utilizing R&D tax credits, the elimination of the “Discovery Rule” in 2001 expanded the definition of R&D to include many activities that these types of firms engage in.

EXAMPLES OF QUALIFYING A/E/C ACTIVITIES INCLUDE

- Green building design/LEED

- Structural engineering to withstand earthquakes, natural disasters

- Alternative material experimentation

- HVAC system design for airflow and energy efficiency

- Plant production system and design

- Plumbing system design for efficient water usage

- Drainstorm/water management design

- High tech equipment installation

- Testing and experimentation

- Electrical system design for efficient power usage

- Testing new concepts and technology

- Developing, implementing or upgrading systems and/or software

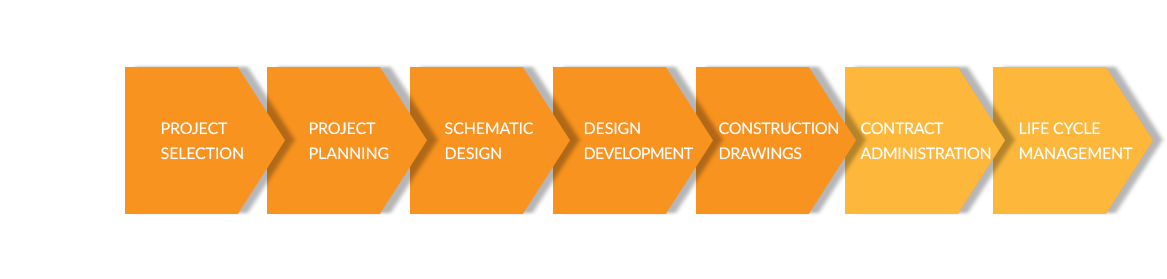

FROM CONCEPT TO PRODUCTION

TYPICAL A/E/C DESIGN APPROACH

R&D tax credits are concerned with activities, not just allocated R&D budgets. Qualified R&D activities generally start at the point of initial project selection and continue through construction drawings. Once a project has been finalized and initiated, R&D no longer applies.

Architecture

Many architectural firms are not aware that activities that they consider part of their day-to-day operations can, in fact, qualify for federal and/or state research and development tax credits. Efforts made to develop new or improved building designs or to increase the functionality, performance, reliability, or quality of a building or structure make a company eligible to receive tax credits.

Client A

- Employees: 18

- Revenue: $1,630,000

- Total Credit: $33,000 **

Client B

- Employees: 65

- Revenue: $18,973,000

- Total Credit: $344,000 **

Client C

- Employees: 167

- Revenue: $51,894,000

- Total Credit: $208,400 *

Federal Only (*) or Federal & State (**)

Engineering

Many companies in the engineering industry may not be aware that the daily tasks that they consider routine may, in fact, qualify for research and development tax credits. Business operations that involve developing new or improved structural, mechanical, and electrical systems that are technological in nature entitle a company to federal research and development tax credits.

Client A

- Employees: 29

- Revenue: $3,214,000

- Total Credit: $84,100 **

Client B

- Employees: 122

- Revenue: $27,217,000

- Total Credit: $462,000 **

Client C

- Employees: 1,123

- Revenue: $216,960,000

- Total Credit: $762,000 **

Federal Only (*) or Federal & State (**)

Construction

Many construction companies are not aware that activities conducted by their engineering and architectural employees may qualify for the R&D tax credit. As the construction industry continues to move towards sustainable design and the development of new and innovative construction techniques, companies in the industry may benefit from an R&D tax credit study.

Client A

- Employees: 1,117

- Revenue: $541,000,000

- Total Credit: $619,000 **

Client B

- Employees: 2,218

- Revenue: $367,000,000

- Total Credit: $596,936 **

Client C

- Employees: 230

- Revenue: $131,000,000

- Total Credit: $146,765 *

Federal Only (*) or Federal & State (**)

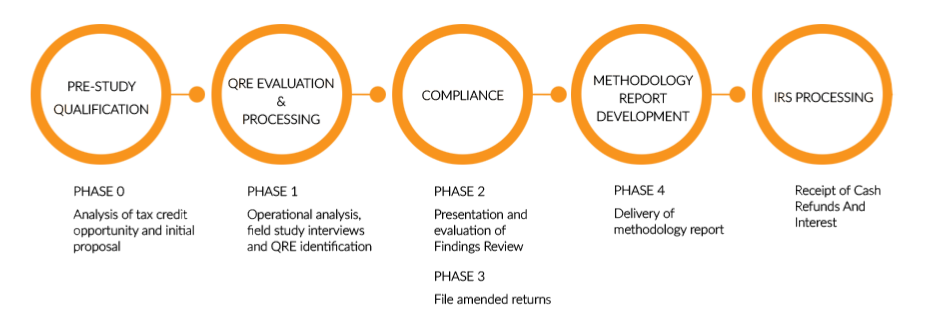

THE APEX ADVISORS R&D TAX CREDIT PROCESS

From study to processing

We utilize a comprehensive process that ensures all possible R&D activities are considered and calculated with accuracy. The Preliminary Assessment is provided to companies at no cost. The estimated duration of all phases is 2 to 3 months.